Russia's tiny banks outshine giants with double the profits and smarter lending

Small Banks Lead Deposit Rate Rankings—But How?

The highest deposit rates today aren't coming from Russia's most recognizable banks. Yet it's no secret that the financial system favors the industry's heavyweights. So how have mid-sized and smaller lenders managed to pull ahead? What keeps them afloat, and where do they turn a profit?

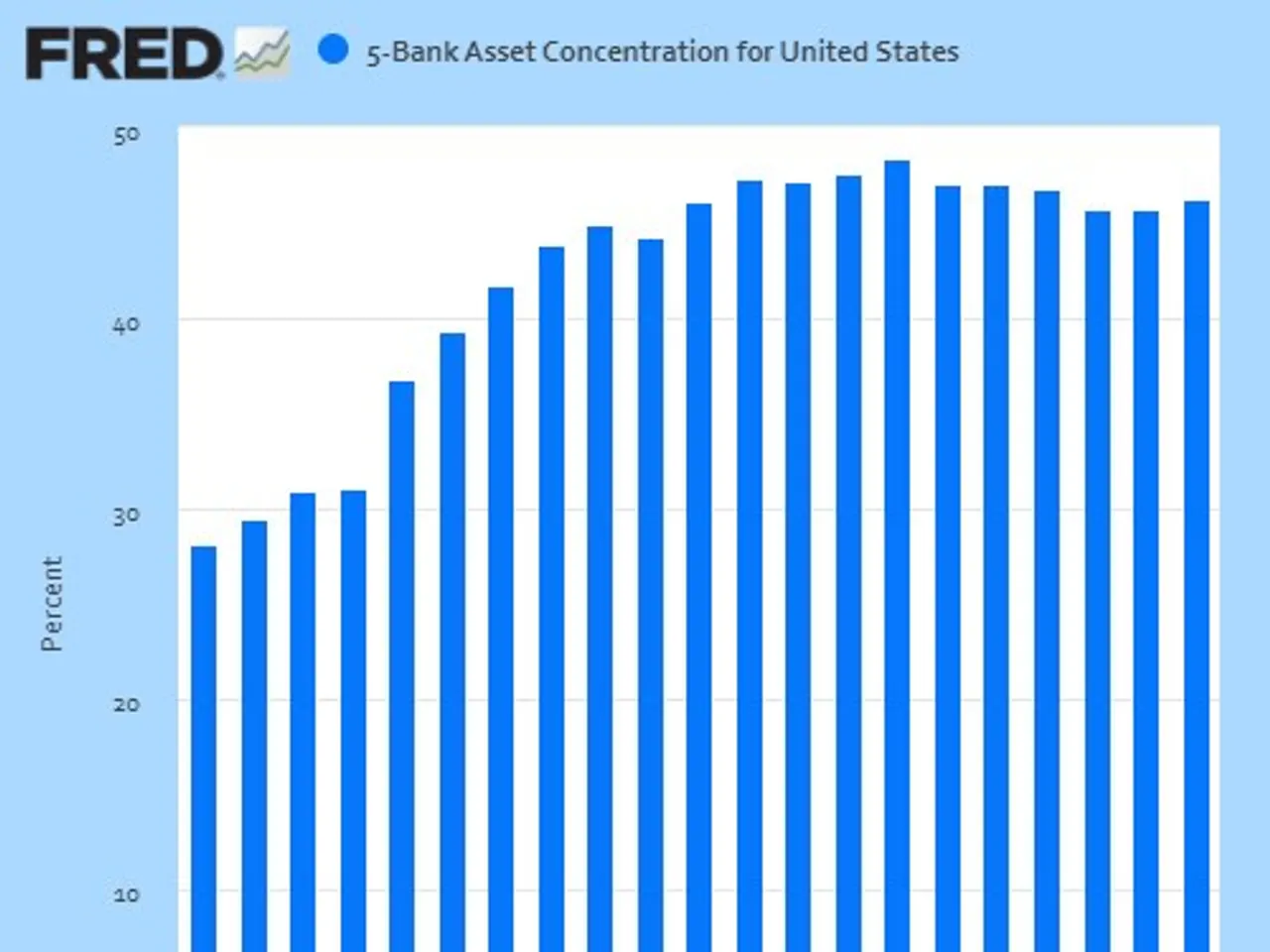

According to the Central Bank, as of February 1, 2026, the combined share of mid-tier and small players (those ranked 101st and below by assets) accounted for just 1.3% of the banking sector's total assets—down from 1.5% a year earlier. A modest figure, to say the least, for a group of over 250 credit institutions. By comparison, the top five banks held 66% of the system's assets (down slightly from 67.4% the previous year).

A bank's size also shapes its asset structure. In smaller lenders, retail loans made up just 9.5% of assets as of early February, with corporate loans (including those to non-bank financial institutions) at 22.1%. In the five largest banks, those figures were roughly 20% and 47%, respectively.

Yet when it comes to return on assets—a key metric for profitability—smaller banks outperform their giant peers. As of early February 2026, their ROA stood at 4.8% (down from 6.9% a year earlier), compared to just 2% for the top five (versus 2.2% the previous year).

To dig deeper, we selected ten mid-sized and small banks offering the most competitive deposit rates. Our list includes Morskoi Bank, Svoi Bank, Realist Bank, NS-Bank, Krokus Bank, Noosfera Bank, Norvik Bank, CMR Bank, and two regional players: Finstar Bank (St. Petersburg) and Kamkombank (Tatarstan).

Small banks are far more active in the interbank market than their larger counterparts—a necessity, given their limited capacity to expand lending.

Rinat Akhmetov, a senior expert at the Center for Macroeconomic Analysis and Short-Term Forecasting (CMASF), notes that trends observed in this sample over the past rolling year (from March 1, 2025, to March 1, 2026) can reasonably be extended to banks outside the top 100 by net assets. In these institutions, retail loans account for roughly 15–16% of net assets—a share that remained stable over the period, mirroring the broader stagnation in consumer lending. Corporate loans make up another 25–27%, tracking a similar flat trajectory.

By contrast, large banks allocate, on average, one and a half times more of their assets to corporate lending.

As Renat Akhmetov explains, the structure of the loan portfolios held by small and medium-sized banks aligns with current trends: retail lending is gradually being replaced by corporate loans, as the Central Bank has taken a tough stance on unsecured consumer credit. The situation is further complicated by the growing share of non-performing and bad loans in the overall retail portfolio. This increase stems from the fact that in the second half of 2023 and early 2024, loans were issued at high interest rates to borrowers who often lacked any credit history. Now, the risks embedded in those loans are beginning to materialize.

When it comes to interbank lending, its share in the balance sheets of small and medium-sized banks remains at around 20% of net assets on average, according to estimates from the Center for Macroeconomic Analysis and Short-Term Forecasting (CMASF). Over the past year, the trend has been uneven: sharp growth in some institutions has been offset by steep declines in others. Overall, as Akhmetov notes, smaller players tend to be more actively engaged in the interbank market compared to major financial institutions. This is because small banks have limited potential to expand corporate lending, often constrained to serving long-standing clients—companies that have maintained relationships with a particular bank either due to shared ownership or because their low credit ratings deter larger banks from working with them.

{kind=link}