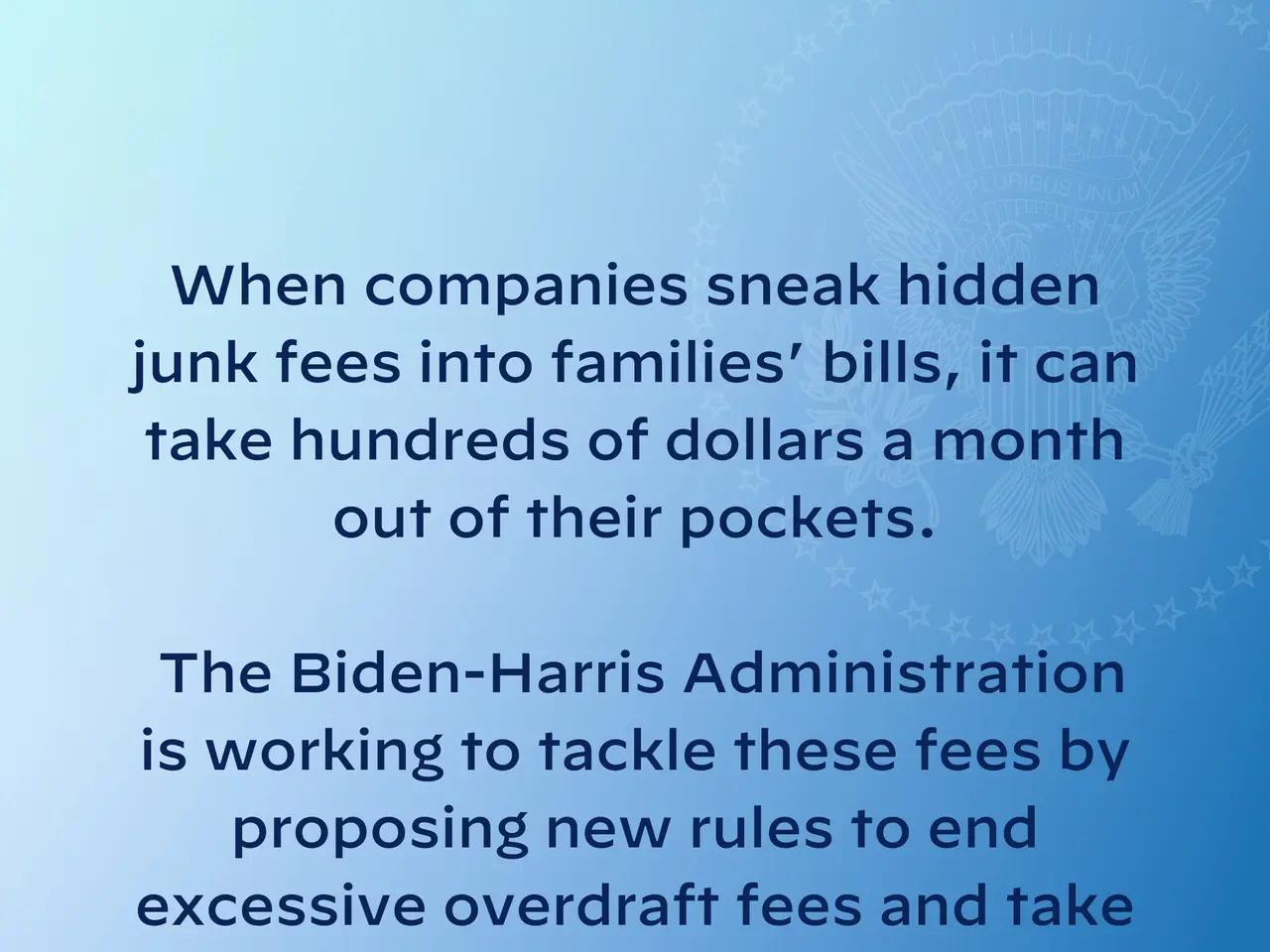

FDIC tightens bank advertising rules to prevent customer confusion by 2025

The Federal Deposit Insurance Corporation (FDIC) has introduced stricter advertising rules for banks and financial institutions. These changes aim to clarify which products carry deposit insurance and which do not. All affected institutions must comply by January 1, 2025. Under the new rules, banks must display the official FDIC sign at every teller window and station where insured deposits are accepted. Digital channels handling deposits must also feature the FDIC's digital sign prominently. New physical branches have 21 days from opening to install the required signage.

ATMs that accept deposits must show the FDIC insured sign, either physical or digital, depending on when the service began. If an ATM offers non-deposit products, it must clearly state on transaction pages that these are not FDIC insured and may lose value.

The rules also require banks to separate FDIC signage from non-deposit product disclosures. Any digital or physical advertising for non-deposit products must explicitly state they are not insured, not deposits, and carry risk. Additionally, banks must notify customers if they leave for non-deposit products on third-party platforms. The updated guidelines take full effect on January 1, 2025. Banks must ensure all deposit-taking locations and digital platforms meet the new signage requirements. Non-compliance could lead to regulatory action, as the FDIC seeks to prevent customer confusion over insured and non-insured products.

{kind=link}